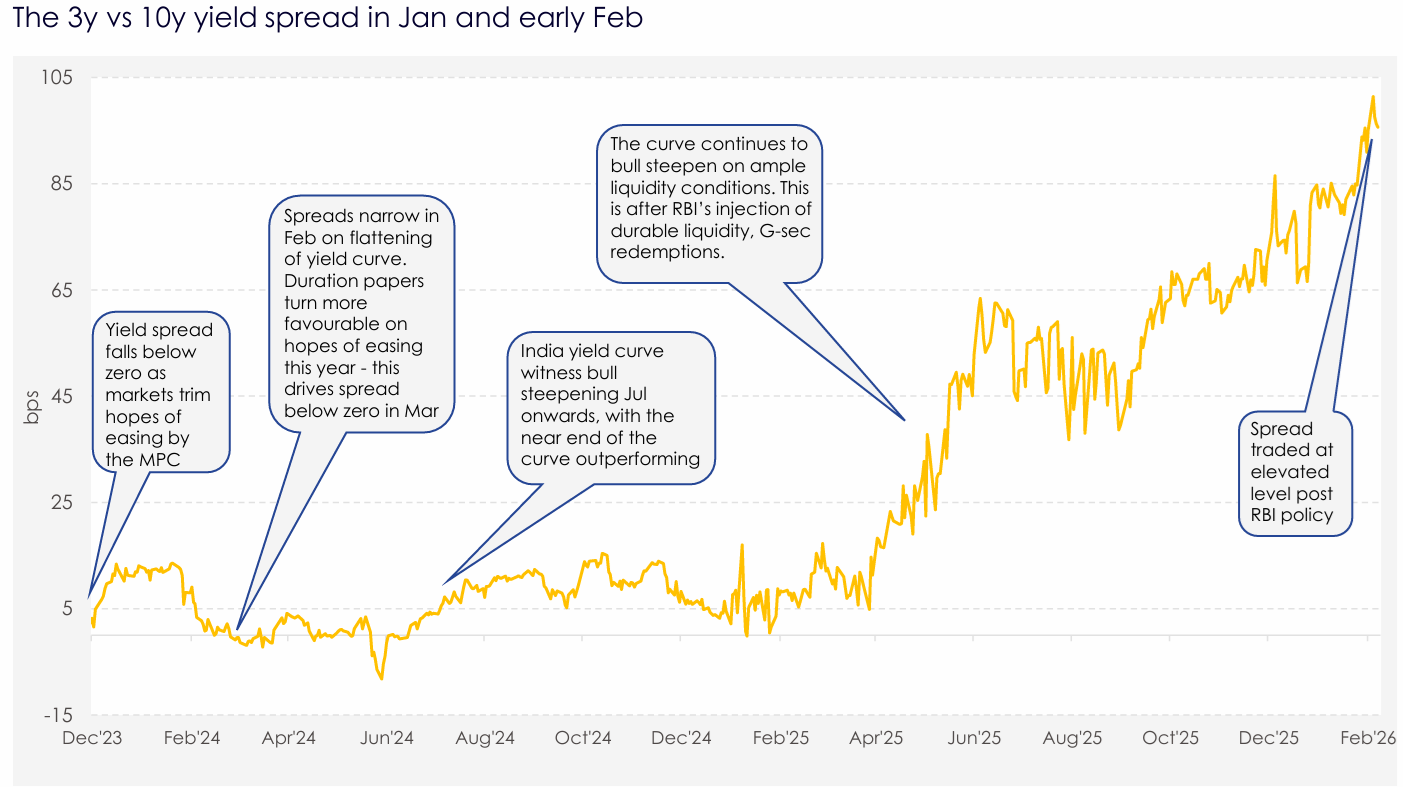

•India G-Sec yields traded mixed to cautious tone within the range of 6.49-6.75%, closing 10 bp higher at 6.69% in January, influenced by various factors: currency movements, OIS rates and expectations of RBI support. •Indian rupee depreciated to a fresh record low of 92/$ on behalf of dollar buying by importers and tracking the bounce in dollar index after US Treasury Secretary Scott Bessent said the US has a strong-dollar policy. •Meanwhile, the 5-year OIS rate surged to fresh 1year high of 6.18% amid sharp fall in INR and cautious ahead of the FY27 Union Budget. •The FY27 Budget, released on Feb 1 also drove the movement in yields, taking them to 6.78%, highest since Jan 17, 2025, after the government's gross market borrowing was pegged at a record INR 17.20 Trln, higher than market expectations of around INR 16.5 Trln. •Throughout Jan and early Feb, market participants were expecting more OMO announcements by the RBI to support the rising yields. The central bank announced further liquidity management measures, including a 90-day VRR of INR 250 Bn on 30 January, a $10 Bn 3-year USD/INR buy/sell swap, and OMO purchases worth INR 1000 Bn across two tranches in January & February, however it didn’t support the local bond market. •Even at the RBI MPC outcome on Feb 6, there was no OMO announcement, rather Governor Malhotra said that the central bank would remain proactive in liquidity management along with keeping the policy rate unchanged at 5.25% and retained the ‘neutral’ stance. •The banking system liquidity had bouts of being in deficit on GST outflows and RBI’s FX intervention; however, it stayed in surplus due to RBI’s liquidity management measure, such as 8-day VRR, OMO purchase auction and FX buy/sell swaps.