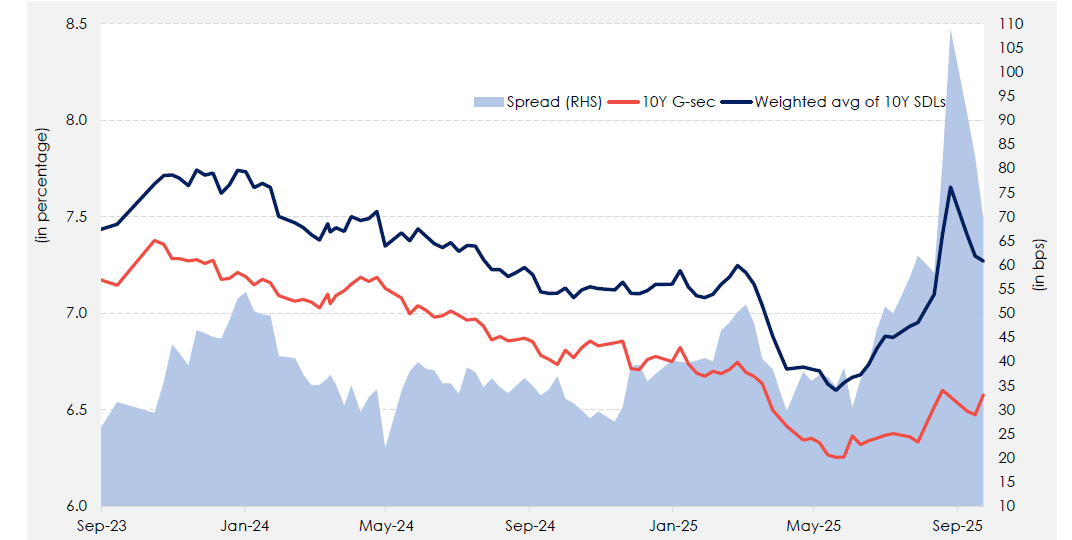

•India G-Sec yields closed 1 bp higher at 6.58% in September, driven by various factors: status quo by the RBI MPC, reduction in government’s H2FY26 borrowing, 25bps rate cut by the Federal Reserve. •The RBI MPC kept the repo rate unchanged at 5.5% with a neutral stance, as expected. It lowered FY26 inflation to 2.6% (from 3.1%) and raised GDP growth to 6.8% (from 6.5%). The decision briefly pushed 10Y yields up to 6.60%, before easing to 6.53% after Governor Malhotra signalled scope for further decline in yields. •The Centre’s H2FY26 borrowing was set at INR 6.77 tn, INR 50 bln below budget. It cut ultra-long (30–50Y) issuance to 29% from 35%, shifting supply to the 10–15Y segment, which made the belly heavier and pushed 10Y yields up to 6.57%. •The States and Union Territories planned to borrow around INR 2.81tn in the Q3FY26, slightly lower compared to Q2FY26 issuance of INR 2.86 tn and a ~12% decline from Q3FY25 issuance of INR 3.20 tn. The lower-than-expected figure triggered some rally in the bond market, with IGB 10Y bond yield falling to 6.49%. •The SDL-GSec 10Y spread narrowed on account of dovish commentary by RBI-MPC leading to expectations for December rate cut, also the reduction in the supply of bonds at Centre and state levels. •Going ahead focus will be on FOMC Oct policy outcome and it is expected to lower fed fund rate by 25bps to 3.75-4.00% from the current 4.00-4.25% to support the labour market despite inflationary pressures