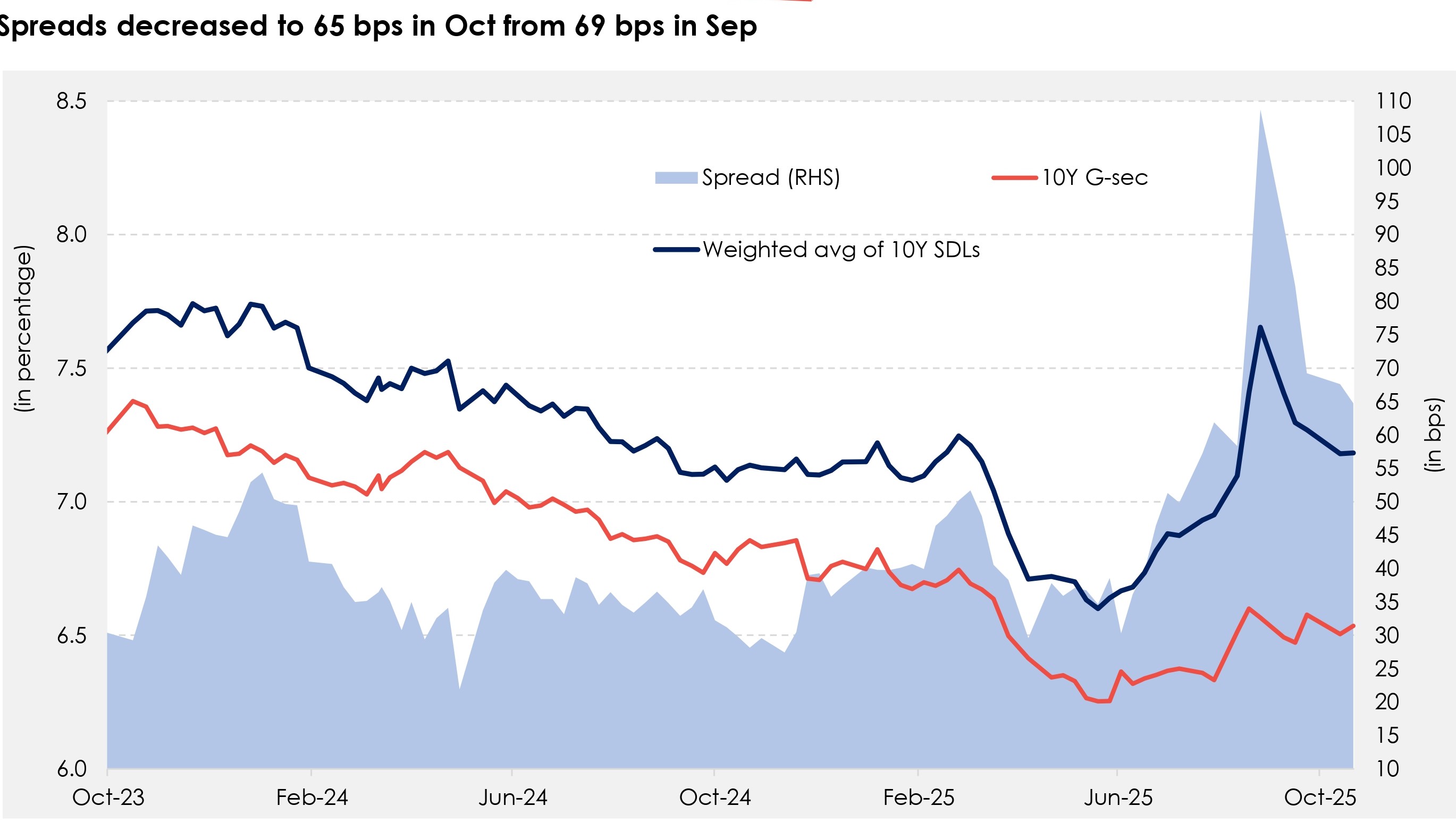

In this edition of Bond Compass, we highlight the key themes for Oct : • India G-Sec yields closed 5bp lower at 6.52% in October, driven by various factors: status quo by the RBI MPC, 25bps rate cut by the Federal Reserve, liquidity crunch due to festive season, weakness in INR. • The RBI MPC kept the repo rate unchanged at 5.5% with a neutral stance, as expected. It lowered FY26 inflation to 2.6% (from 3.1%) and raised GDP growth to 6.8% (from 6.5%). The decision briefly pushed 10Y yields up to 6.60%, before easing to 6.53% after Governor Malhotra signalled scope for further decline in yields. • As expected, the FOMC announced a 25-basis point interest rate cut to the range of 3.75%-4.00% but suggested that another cut in December is not a foregone conclusion. This led to a sharp spike in UST yields, impacting IGB 10Y bond yield. • The banking system liquidity grappled with liquidity conditions being by festival demand for currency notes. However, RBI intervened in the market by conducting VRR auctions.