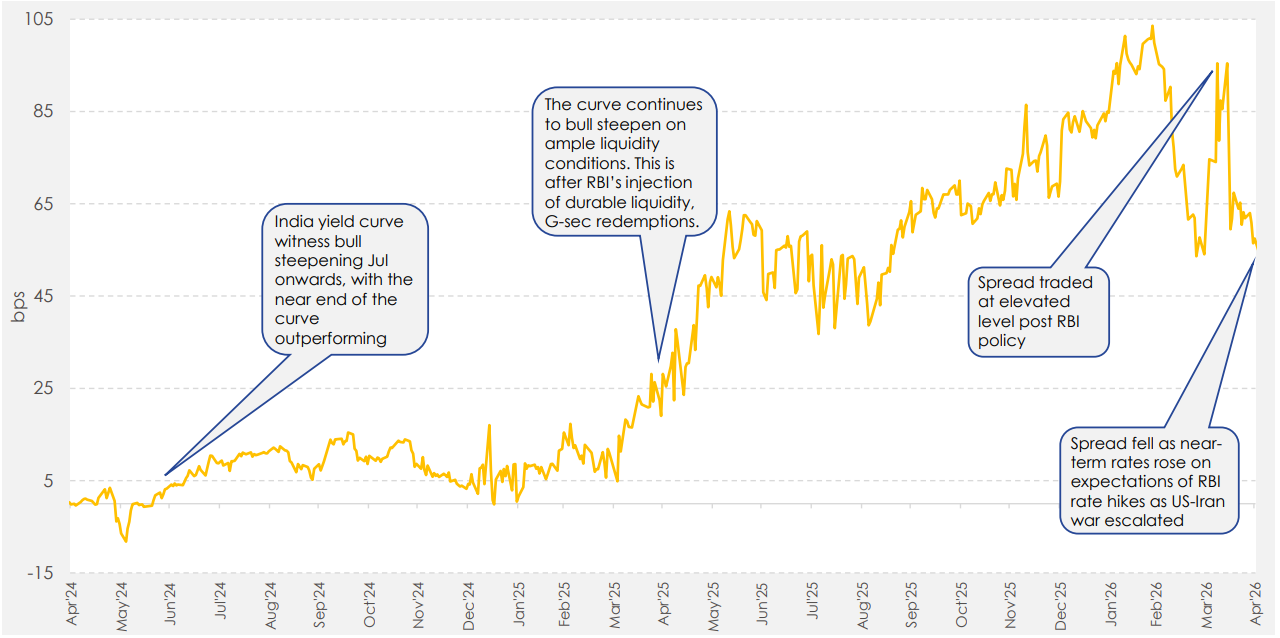

•India Gsec yields stayed ranged bound in between 6.87-7.13% to end flat at 7.01% amidst concerns over West Asia conflict. The benchmark yield showed some downward correction on reports of war ending soon, but delay in formal peace deal, kept local yield afloat. •INR hit record low of 95.33/$ at the end of Apr’26 on strong outflows from local equities. To limit the sharp depreciation in INR, contain excessive risk-taking, reduce speculative pressures, RBI announce additional measures in April such as restricted Authorised Dealers from offering INR NDF contracts to residents and non-residents and tightened rules on cancellation and rebooking of FX derivative contracts. These measures led to a surge in INR to a two-week high of 92.82/$, however it was short-lived. •Brent crude oil July futures continued to be elevated trading within a range of $86-120/barrel as US-Iran hostilities continued amid fears of supply disruption due to the blockade of Strait of Hormuz.